Binary Logistic Regression in Python

Blog Tutorials

Predict outcomes like loan defaults with binary logistic regression in Python!

Binary Logistic Regression in Python

Binary logistic regression models the relationship between a set of independent variables and a binary dependent variable. It is useful when the dependent variable is dichotomous in nature—for example: death or survival, absence or presence, pass or fail. In logistic regression, the dependent variable is a binary variable coded as 1 (yes, success, etc.) or 0 (no, failure, etc.). The logistic regression model essentially predicts P(Y=1) as a function of the independent variables X. The independent variables can be categorical or continuous (e.g., gender, age, income, region, and so on). Binary logistic regression models a dependent variable as a logit of p, where p is the probability that the dependent variable takes the value “1”.

Statistical Model – For k Predictors

(Replace image here: alt="Binary Logistic Regression in Python Model formula")

The statistical model in binary logistic regression can be written as follows:

where

p : Probability that Y=1 given X

Y : Dependent Variable

X1,X2,…,Xk : Independent Variables

b0,b1,…,bk : Parameters (coefficients) of the model

The parameters (b0 to bk) are typically estimated using the maximum likelihood method. The left-hand side of the equation ranges from −∞ to +∞.

Case Study – Modeling Loan Defaults

To illustrate binary logistic regression, consider a bank’s scenario:

The bank has demographic and transactional data of its loan customers.

The goal is to develop a model predicting whether a customer will default or not on a new loan.

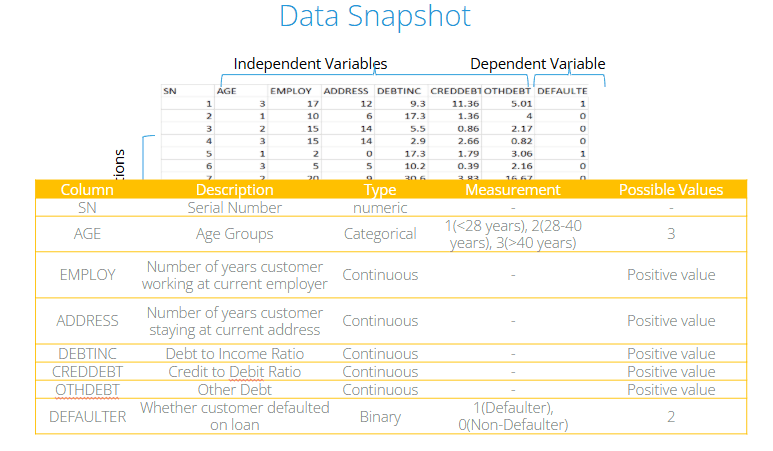

We have a sample of 700 loan customers. The independent variables used are:

Age group

Years at current address

Years at current employer

Debt to income ratio

Credit card debt

Other debt

All these are collected at loan application. The dependent variable is the observed status (1 = defaulter, 0 = not defaulter) after the loan is disbursed.

Below is a snapshot of the data. The dependent variable is binary, while the independent variables are a mix of categorical and continuous types.

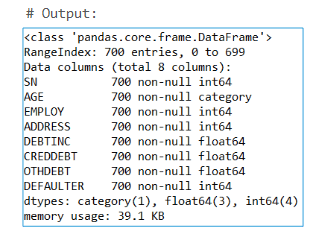

Importing and Inspecting the Data

You might notice from the output that Age appears as an integer, but for our analysis, we need it to be a categorical variable (since we’re considering age groups). If we leave Age as a numeric variable, Python will treat it incorrectly as a continuous variable.

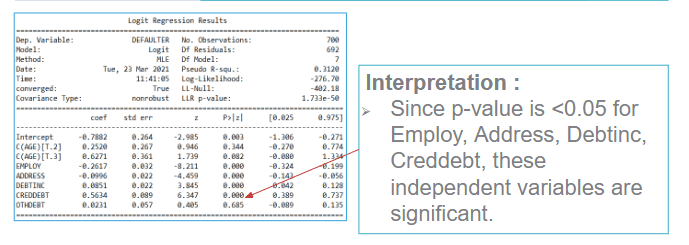

Fitting the Logistic Regression Model

In a logistic regression, we use the logit link function. Below is the initial model that includes all the variables we want to test:

From the summary, we can see the significance (p-values) of each variable. The variables EMPLOY, ADDRESS, DEBTINC, and CREDDEBT are statistically significant (p-value < 0.05).

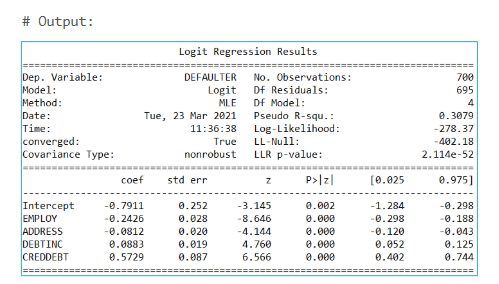

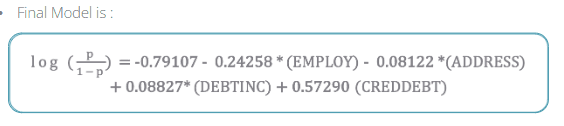

Re-running the Logistic Regression With Significant Variables

We now refine our model by dropping the insignificant variables:

In this refined output, all the independent variables are significant, and the signs of the coefficients make sense. This final model can be used for further analysis.

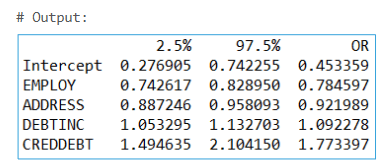

Odds Ratios in Python

Odds ratios help interpret the effect of each independent variable on the probability of being a defaulter. After fitting the final model, we can obtain the parameter estimates along with confidence intervals, and then exponentiate (antilog) those estimates to get odds ratios.

If an odds ratio’s confidence interval does not include 1, that variable is considered significant. For example, if CREDDEBT has an odds ratio of 1.77, then for a one-unit increase in CREDDEBT, the odds of defaulting increase by a factor of 1.77, holding other variables constant.

Predicting Probabilities in Python

After finalizing our model, we can generate predicted probabilities of default for each observation:

The last column in bankloan now holds these predicted probabilities.

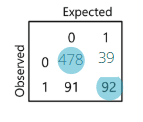

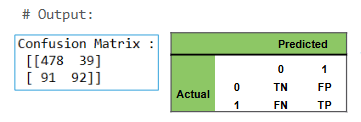

Classification Table

To measure how well the model performs, we set a cutoff (threshold) for classifying whether a loan defaults or not. Often, we start with a threshold of 0.5:

If the predicted probability > 0.5, we classify the customer as a “defaulter” (1).

Otherwise, classify as “not defaulter” (0).

We then compare these predictions to the actual observed values (defaulters vs. not defaulters). This forms the classification table (also called a confusion matrix). The accuracy rate is the percentage of correct predictions, while the misclassification rate is the percentage of incorrect predictions.

Classification Table Terminology

Sensitivity: The percentage of correctly predicted events (defaulters). Mathematically, it is TPTP+FN\frac{TP}{TP + FN}.

Specificity: The percentage of correctly predicted non-events (non-defaulters). Mathematically, it is TNTN+FP\frac{TN}{TN + FP}.

False Positive Rate: The percentage of non-events wrongly predicted as events.

False Negative Rate: The percentage of events wrongly predicted as non-events.

Sensitivity and Specificity Calculations

Different threshold values can yield different levels of accuracy, sensitivity, and specificity. You can compare these values for various cutoffs (e.g., 0.3, 0.4, 0.5) to choose the best threshold.

Classification Table in Python

Let’s generate the confusion matrix in Python:

The confusion matrix (classification table) compares observed defaulters (1) vs. predicted defaulters (1), and observed non-defaulters (0) vs. predicted non-defaulters (0).

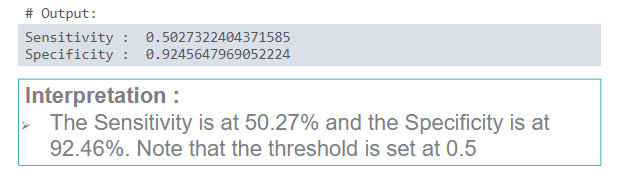

Sensitivity and Specificity in Python

If the sensitivity is low (e.g., 50.27%), you might try adjusting the threshold to improve the model’s ability to detect defaulters (true positives).

Precision & Recall

Precision: Of the predicted positive cases, what proportion was truly positive?

Recall: Of the actual positive cases, what proportion was predicted correctly?

These metrics are routinely used to evaluate classification models.

Classification Report

(Replace image here: alt="Classification Report")

The classification_report function in Python provides recall, precision, and accuracy, all in one place:

Interpretation :

Recall is 50% & Precision is 70%.

Accuracy is 81%.

This gives us a quick overview of how well the model is classifying defaulters and non-defaulters.

Quick Recap

We introduced how binary logistic regression models the probability of a binary outcome and applied it to a real-world banking case study aiming to predict loan defaults. Using Python, we demonstrated how to import and inspect the data, fit an initial logistic regression model, identify significant variables via p-values, and refine the model by including only those significant variables. We then showed how to calculate and interpret odds ratios, predicted probabilities, classification tables, sensitivity, specificity, precision, and recall. Altogether, this provides a comprehensive blueprint for performing binary logistic regression in Python and effectively interpreting the resulting classification model.